If you earn above the national average, retirement planning looks different for you than it does for most. The standard...

The idea that self-employed people struggle to get a mortgage is one of the most stubborn myths in the UK...

Being your own boss brings enormous freedom, but it also removes the safety net that employed people often take for...

When seeking financial advice, one of the first decisions you may face is whether to pay for a one-off piece...

If your mortgage fixed rate is due to end within the next six to nine months, now may be the...

If your family relies on your income, life insurance can provide valuable financial protection should the worst happen. However, many...

Buying a property is one of the biggest financial decisions many people make and one of the first questions buyers...

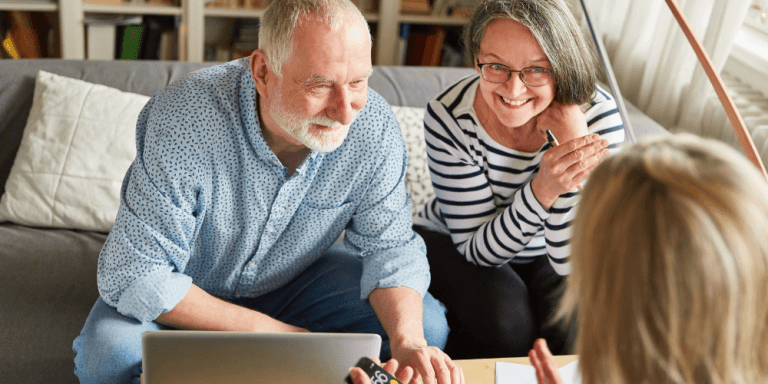

Estate planning is often something people intend to do, but later. It sits on the to do list alongside updating...

Many people assume they are financially protected if their income suddenly stops. However, when asked exactly what their insurance policies...